Consumer Trends in the Automotive Industry

Consumer Trends in the Automotive Industry: How Buyers Are Reshaping the Market in 2024–2026

Introduction: Why Consumer Trends Matter for Automotive Businesses

If you’re in the business of selling, financing, or servicing cars, understanding the forces reshaping buyer behaviour is no longer optional. It’s the difference between capturing market share and watching it slip to more agile competitors.

The consumer trends in the automotive industry today are fundamentally altering how vehicles move from production lines to driveways. Expectations around price transparency, sustainability, and digital convenience are directly reshaping product mix, retail formats, and marketing strategies across the global automotive industry. Businesses that fail to adapt will find themselves stuck with aging inventory, misaligned marketing messages, and shrinking margins.

The context heading into 2026 is complex. Global light-vehicle sales have largely recovered from COVID-19 disruptions, and supply chain normalisation continues, but persistent cost-of-living pressures are weighing heavily on purchasing behaviour. In the EU, battery-electric vehicles accounted for approximately 17.4%% of new-car sales in 2025. Meanwhile, EV penetration in the US has slowed and used-car volumes are growing faster than new in many mature markets. Average new-vehicle list prices hit $49,700 in November 2025, up 0.7% year-over-year, driven by accelerated rollout of higher-priced 2026 model-year vehicles.

This article will walk automotive businesses through the key consumer trends — brand loyalty erosion, powertrain preferences, digital-first journeys, pricing sensitivity, connectivity expectations, and evolving ownership models and show you how to adapt their commercial strategies accordingly.

At-a-Glance: Key Trends Covered in This Article

- Motivation-based buyer segmentation is replacing legacy demographic personas

- Hybrid vehicles are gaining traction as consumers seek practical electrification without charging anxiety

- Omnichannel experiences are table stakes; fragmented online and in-store workflows kill deals

- Connected features and software-defined vehicles are opening new lifecycle revenue streams

From Demographics to Motivations: How Car Buyers Are Redefining Loyalty

Classic brand loyalty is eroding faster than many manufacturers anticipated. In recent European surveys, over 60% of buyers say they are willing to switch brands when purchasing their next vehicle. Similar patterns are visible in US and Chinese markets, where today’s car buyers prioritize specific outcomes over badge allegiance.

The shift is fundamental: car buyers are now segmenting themselves more by “why” than by age, gender, or household income. Consumer behaviour has become motivation-driven, with buyers moving fluidly between priorities depending on life stage, economic conditions, and the specific vehicle type they’re considering.

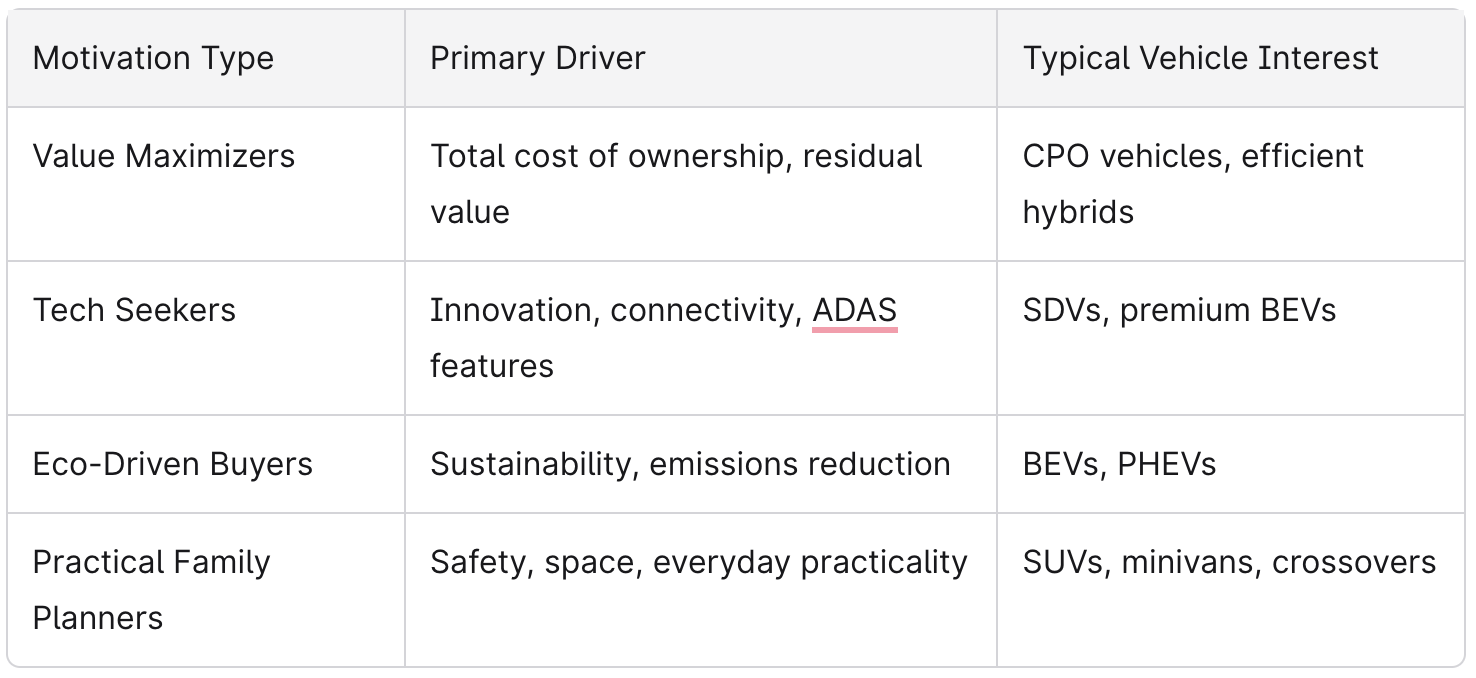

Four Archetypal Buyer Motivations

A single shopper can shift between these motivations across their buying journey. Someone researching a BEV for environmental reasons may ultimately choose a hybrid when charging infrastructure concerns surface.

Lifestyle shifts are amplifying this fluidity. Urbanisation, remote and hybrid work arrangements post-2020, and the rise of multi-car households are changing what “primary vehicle” means. Many consumers now treat their vehicle portfolio differently, one car for commuting, another for weekend trips, which affects which segment wins in any given transaction.

For Automotive Businesses: Building Motivation-Based Segments

- Use first-party data from website behaviour, showroom visits, and service history to identify buyer motivations

- Track intent signals across devices; configurator interactions, financing calculator usage, trade-in inquiries

- Analyse trade-in history to understand what vehicles customers are leaving and why

- Survey existing customers on purchase drivers to validate segment assumptions

- Train sales teams to diagnose motivation early in conversations rather than defaulting to demographic assumptions

The companies building data intelligence capabilities to understand these shifts will have a competitive edge in converting more leads and building customer loyalty that transcends individual transactions.

EVs, Hybrids and ICE: Powertrain Choices Behind the Headlines

The powertrain landscape in 2024–2026 defies simple narratives. Battery electric vehicles are still growing globally, but well below earlier projections. Regional differences are stark: Norway exceed 90% BEV share, while the US hovers around ~8%.

The real story is the hybrid resurgence. In 2023–2024, HEVs grew multiple times faster than BEVs in several markets as consumers sought better total cost of ownership without charging anxiety. This pragmatic turn is reshaping how OEMs and dealers should think about inventory and marketing.

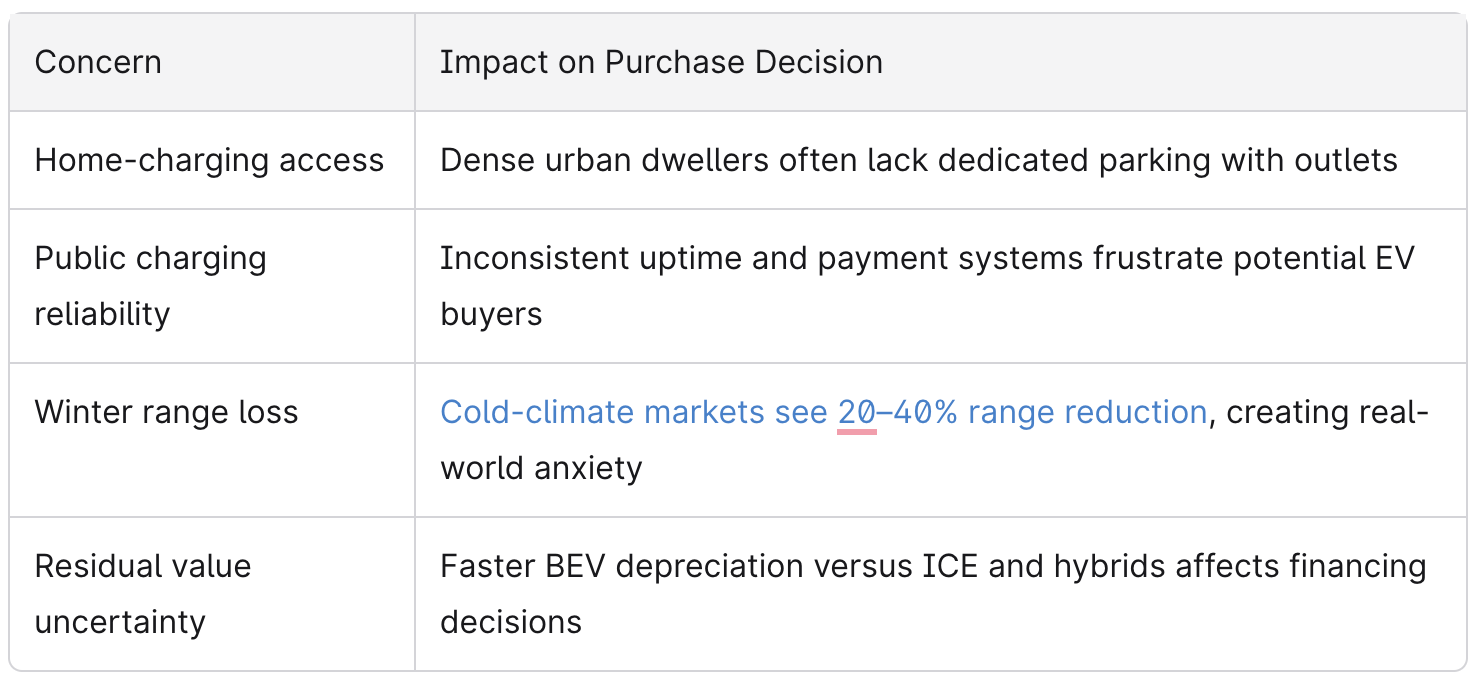

What’s Driving Consumer Powertrain Concerns

The shift toward hybrids positions OEMs which pair electrification with flexible strategies as outperformers.

*Cold-climate markets see 20–40% range reduction.

For OEMs, Dealers, and Leasing Companies

- Maintain a balanced mix of BEV, PHEV, HEV, and efficient ICE through at least 2028

- Tailor stock to local infrastructure realities, charging-point density, average commute lengths, and climate

- Use registration data by powertrain to inform regional model mix decisions

- Position environmental messaging for eco-driven segments while emphasising cost-of-ownership for value maximisers

- Prepare sales staff to explain the practical trade-offs between powertrains without pushing a single solution

The market is telling you that many consumers want electrification on their terms. Listen to that signal.

Digital-First Journeys: Omnichannel Car Buying and Ownership

In most markets, over 90% of buyers research online before visiting a showroom. A growing minority of younger buyers are willing to purchase a vehicle without a physical test drive if they trust the brand and return policy.

The path to purchase now spans multiple touchpoints: OEM configurators, independent review sites, YouTube and TikTok creators, marketplace listings, dealer websites, and messaging apps. Consumers expect seamless transitions between these channels, picking up where they left off, regardless of device or location.

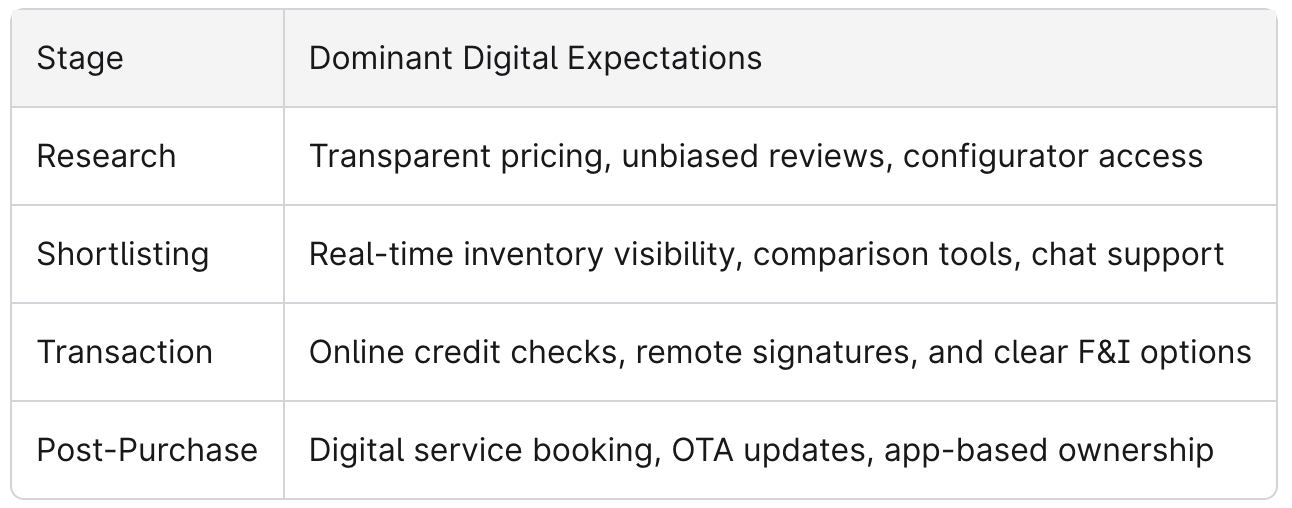

The Four Stages of the Digital Car-Buying Journey

The 2025 Cox Automotive Drivers of Car Shopping Satisfaction Study found that peak satisfaction occurs when customers feel in control across research, comparisons, and paperwork. Fragmented workflows where online progress disappears when a customer walks into the showroom kill deals and damage brand perception.

Priority Capabilities for 2024–2026

- Deploy unified CRM across dealer groups that captures online behaviour alongside showroom interactions

- Ensure consistent pricing and incentives online versus offline to eliminate customer frustration

- Offer virtual consultations for buyers who want expert guidance without immediate showroom visits

- Build clear hand-off protocols between digital and showroom teams so no customer starts from scratch

- Enable near-complete online workflows: reservation, F&I pre-approval, trade-in appraisal

Car dealerships that provide these capabilities are closing transactions faster and at lower acquisition costs. While fully online sales remain a small share, the expectation of online workflow availability is now universal. Automotive marketing must reflect this reality, driving traffic to experiences that convert, not just landing pages that inform.

Price Sensitivity, Financing and the Rise of the Used and CPO Market

Inflation and higher interest rates have pushed monthly payments to levels that make affordability the primary constraint for many households. This shift is reshaping the entire market, not just the budget segments.

The price gap between new and used vehicles is widening, and prices for certain segments, such as compact SUVs, softened in late 2024. Meanwhile, affordable used cars are becoming scarce. Sedans from prior years are nearly vanishing from dealer lots, keeping prices elevated for entry-level trades.

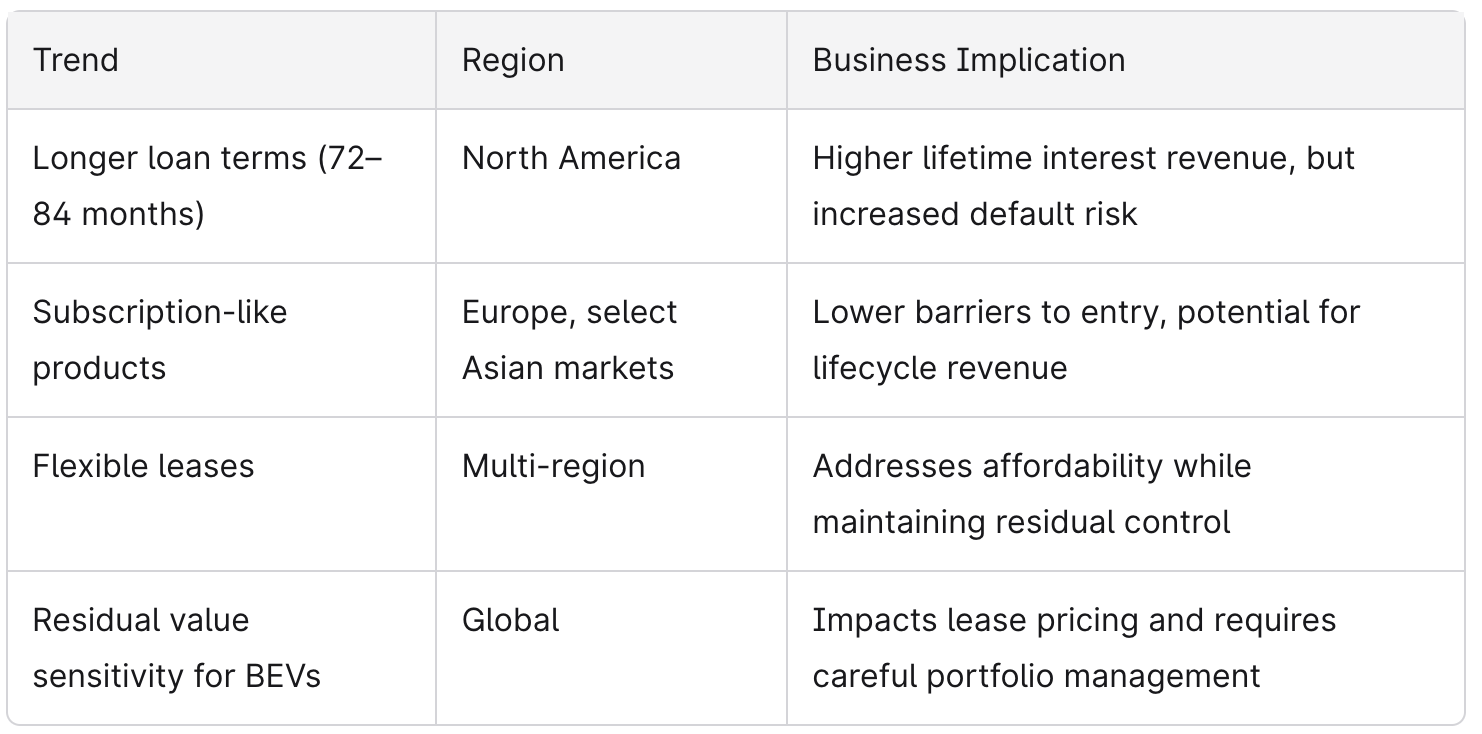

How Financing Behaviour Is Shifting

Many consumers now treat “new vs. used vs. nearly-new” as a single decision set. They compare 1-3 year old CPO vehicles directly with new cars under heavy incentives. This value-driven comparison shopping requires dealers to present compelling value propositions across their entire inventory.

For OEMs, Dealers, and Captives

- Build clearer value propositions for used and CPO: extended warranties, transparent reconditioning standards, and digital vehicle history

- Use data to price inventory dynamically by region, trim level, and local demand

- Communicate the total cost of ownership, not justthe sticker price, in all customer-facing materials

- Consider how subscription and flexible lease products can capture price-sensitive buyers who might otherwise exit the market

- Monitor residual value trends for BEVs closely when structuring lease offers

The businesses winning in this environment are those treating car sales as a portfolio problem, optimising across new, CPO, and wholesale channels rather than fixating on any single category.

Connected, Software-Defined Vehicles: What Consumers Expect and Will Pay For

Connectivity and software now heavily influence perceived value, particularly among young buyers, even when they choose ICE or hybrid powertrains. The connected vehicle is no longer a luxury differentiator; it’s a baseline expectation.

Feature Clusters That Consistently Test Well

- Seamless smartphone integration (Apple CarPlay / Android Auto)

- Advanced driver-assistance systems: adaptive cruise, lane-keeping, automatic emergency braking

- Over-the-air software updates that improve the vehicle after purchase

- Integrated navigation with live traffic and charging or fuel pricing

- Voice assistants with natural language processing

By 2031, an estimated 28 million vehicles will feature GenAI chatbots, opening new subscription revenues from ADAS features, OTA updates, and connected services. Interior upgrades, soft-touch surfaces, next-gen infotainment, motorised and heated seats are proliferating, elevating perceived value and helping justify higher transaction prices.

Willingness to pay is not uniform. Buyers often expect safety-related ADAS as standard, viewing it as a cost of entry rather than a premium add-on. However, they’re more prepared to pay recurring fees for convenience, entertainment, or performance-enhancing software features that feel discretionary and personal.

Strategic Implications of the SDV Trend

- Design modular hardware platforms that support software differentiation over the vehicle lifecycle

- Draw a clear line between one-time hardware options and subscription-based software features

- Simplify subscription menus, consumer confusion kills conversion rates

- Treat connected features as part of the ongoing customer relationship, not a one-off upsell at purchase

- Partner with technology providers for advanced technology integration while retaining brand control

Example: A mid-size SUV launching in 2025 might offer a base ADAS bundle including adaptive cruise and lane-keeping as standard, with an optional monthly upgrade unlocking hands-free driving on mapped highways. The base builds trust; the subscription captures lifestyle revenue.

Dealers can leverage this shift by positioning themselves as ongoing service providers rather than transaction facilitators. Insights from connected-vehicle data, driving patterns, service needs, and feature usage create opportunities for proactive engagement and loyalty-building.

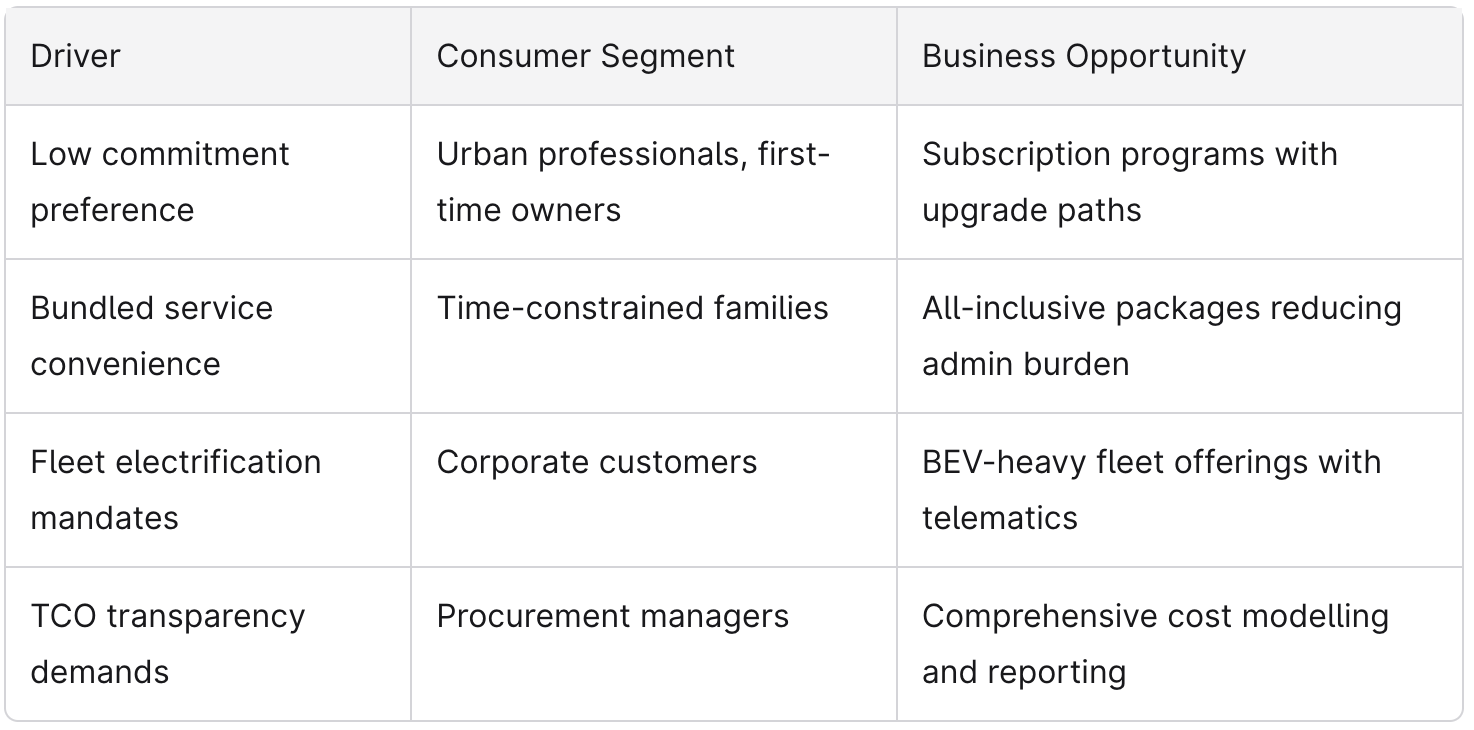

New Ownership and Mobility Models: From Single Purchase to Lifecycle Relationship

Urban consumers, younger cohorts, and business fleets are rethinking car access. Interest in flexible leases, short-term subscriptions, car sharing, and employer-provided mobility benefits is growing, though private ownership remains dominant.

Subscription pilots in Europe and North America have demonstrated strong customer uptake among those who value low commitment and bundled services. These programs typically include insurance, maintenance, and roadside assistance in a single monthly payment, removing friction from the ownership experience.

What’s Driving the Shift

Fleets and corporate customers are pushing for electrification, connected telematics, and total cost of ownership transparency. This indirectly shapes consumer offers more BEV variants, bundled home charger installation, and integrated energy tariffs as OEMs develop capabilities for B2B customers that eventually flow into retail channels.

Strategic Options for Dealers and OEMs

- Launch branded subscription programs that complement traditional purchase and lease

- Collaborate with mobility platforms to capture usage rather than ownership demand

- Offer “upgrade paths” during the life of a lease, allowing customers to switch vehicles as needs change

- Build digital portals that centralise finance, insurance, and service for a unified customer experience

- Track new KPIs: active users, churn, subscription ARPU, alongside traditional sales metrics

Example: A European OEM offers a monthly all-inclusive program covering insurance, maintenance, and roadside assistance. Customers can swap vehicles quarterly, choosing from a curated selection of sedans, SUVs, and EVs. A dealer group in the same market partners with this program, earning commissions on enrollments and maintaining the service relationship.

The shift from one-time sale to lifecycle revenue requires closer coordination between sales, after-sales, finance, and product teams. Siloed operations can’t deliver the seamless experience that subscription and flexible models demand.

Implications for Automotive Marketing, Retail and Product Strategy

The trends discussed motivation-based segments, mixed powertrain demand, digital-first journeys, price sensitivity, connected features, and new ownership models interlock to reshape how vehicles should be designed, priced, and sold. No single trend operates in isolation; success requires addressing them as an integrated system.

The automotive sector is experiencing a fundamental shift in how value is created and captured. Manufacturers that cling to legacy assumptions about brand loyalty, channel separation, or product-only revenue models will find themselves outmanoeuvred by more agile competitors. The road ahead rewards businesses that treat evolving consumer expectations as the primary input to strategy, not an afterthought.

Strategic Priorities for OEMs and Retailers: 2024–2026

Build integrated data platforms that join online behaviour, showroom visits, and service history into unified customer profiles. The companies with the best data intelligence will make better decisions about inventory, pricing, and marketing allocation.

Rebalance marketing spend toward measurable, performance-based digital channels while maintaining high-impact brand building. Automotive marketing must demonstrate ROI while still investing in the brand equity that supports premium pricing.

Equip frontline staff with tools and training to explain EVs, hybrids, connectivity packages, and flexible ownership products clearly. Consumer confusion at the point of sale kills deals and damages long-term relationships.

Action Checklist for Automotive Businesses

- Audit current digital capabilities against the omnichannel expectations outlined above

- Pilot smaller, fast-cycle experiments, new digital funnels, subscription offers, targeted EV education campaigns and scale what works

- Monitor external signals: regulatory changes (emissions and EV mandates), local charging and fuel infrastructure development, consumer sentiment around economic conditions

- Invest in AI-driven tools for fraud mitigation, dynamic pricing, and personalised offers

- Align internal incentives so that sales, after-sales, and finance teams share ownership of customer lifetime value

The companies most aligned with consumer trends in 2026 will capture not only new-vehicle sales but also software revenue, service relationships, used vehicles, and lifetime customer value. To stay competitive, start adapting today. The market won’t wait, and neither will the consumers driving these changes.

The latest trends point clearly: those who invest in innovation, embrace flexibility, and build around customer expectations will own the future. Those who don’t will find themselves competing on price alone, a race to the bottom that benefits no one.

Ready to activate high-impact and performance-driven automotive marketing? Driftrock powers lead generation for 65% of the automotive industry, helping 80+ brands across 24 markets generate over 1.7 million leads annually and enable £1.8 billion in vehicle sales. Our platform automatically validates leads, routes them to the right dealers, and tracks performance from click to sale, saving marketing teams an average of 3 years and 11 months in time, whilst cutting costs by up to 50%.

Whether you're looking to increase lead volume, improve conversion rates, or prove ROI, we've built the tools automotive marketers actually need. Book a demo to see how we can help you drive better results from your marketing spend.