Automotive Industry Outlook: Growth & Trends

Executive summary: what vehicle businesses must plan for now

The automotive industry is entering a period of structural recalibration that will test the strategies, margins, and capital allocation decisions of every player across the value chain. For OEMs, dealer groups, leasing companies, and suppliers, the 2025–2030 window presents a complex operating environment shaped by economic headwinds, policy volatility, and intensifying global competition. The U.S. new-vehicle market is projected to stabilize at approximately 16 million units annually—a sustainable baseline driven by genuine consumer demand rather than artificial incentive programs. Meanwhile, electric vehicle market share is expected to contract to around 6% in 2026 as federal tax credits expire, forcing a recalibration of electrification timelines across the industry.

The headline pressures facing industry leaders are clear:

- High interest rates continuing into 2025 are compressing retail demand and extending vehicle ownership cycles

- Slower-than-planned EV adoption is stranding capital invested in battery plants, dedicated platforms, and charging infrastructure

- Escalating trade tensions and tariffs, particularly involving the U.S., China, Mexico, and the EU, are disrupting supply chains and raising production costs

- Intensifying competition from Chinese OEMs is threatening pricing power and market share in emerging markets and increasingly in Europe

This article is written specifically for businesses operating in the automotive value chain—from original equipment manufacturers and Tier 1 suppliers to dealer networks and fleet operators. The focus is on strategy, margins, and capital allocation, not consumer purchasing advice.

What this means for your business in 2025:

- Protect cash and prioritize profitability over volume

- Re-prioritize capex toward flexible platforms and regionalized production

- Diversify supply chains and build scenario-planning capabilities for regulatory changes

Macro and economic trends shaping the 2025 auto market

The 2025 macro environment presents a challenging backdrop for automotive businesses. Stubbornly high interest rates, sticky inflation across key input categories, and the slow normalization of supply chains after years of COVID-era disruptions are creating a market where growth is harder to achieve and margins are under pressure. Understanding these dynamics is critical for anyone managing inventory, setting production forecasts, or allocating capital.

Interest rate levels in 2024–2025 are directly impacting every layer of the auto market. Average new-vehicle loan APRs remain elevated, pushing monthly payments beyond affordability thresholds for many buyers. This dynamic is particularly acute for price-sensitive consumers, who are increasingly being diverted to used vehicles and off-lease alternatives. For dealers, this translates into longer days-to-turn on higher-priced inventory and increased pressure to offer incentives that compress margins. Fleet renewal cycles are also extending as commercial buyers face higher financing costs on vehicle acquisitions.

Inflation in key inputs—steel, aluminum, lithium, and labor—continues to flow through into vehicle prices. While new-vehicle transaction prices have stabilized after years of rapid escalation, they remain elevated relative to pre-pandemic levels. For fleet operators and leasing companies, this inflation is reshaping total cost of ownership calculations and forcing harder decisions about vehicle specifications and replacement schedules.

Global production volumes tell an important story. Compared to 2019 pre-pandemic baselines, the industry has not fully recovered its capacity utilization. North American automotive output is declining as higher prices cool consumer appetite, and global light-vehicle production is projected to contract in 2026, constrained primarily by U.S. tariffs and trade policy uncertainty. For suppliers, this means order books remain volatile and long-term planning is complicated by demand uncertainty.

The market is also experiencing a structural shift in mix. Longer ownership cycles and elevated monthly payments are pushing buyers toward used vehicles, altering the balance between new and used, retail and fleet. Approximately 400,000 additional lease returns are expected to replenish the used-vehicle shopper pool in 2026, providing price-sensitive consumers with affordable alternatives. For dealers and remarketing operations, this influx of off-lease inventory represents both opportunity and competitive pressure on new-vehicle sales.

Policy, tariffs, and regulatory risk for automotive businesses

Regulatory uncertainty has moved from a background compliance concern to a core strategic variable for OEMs, importers, and suppliers. The combination of trade tensions, emissions mandates, and shifting political landscapes means that businesses can no longer treat policy as a stable input to planning. Instead, it must be modeled as a source of significant risk and potential opportunity.

Trade policy is reshaping landed costs and sourcing decisions across the industry. The Trump administration’s tariff measures have created particular pressure on Japanese and South Korean automakers caught between tariff exposure and intensifying global competition. North American output is declining as higher vehicle prices resulting from tariff exposure cool consumer appetite. The early 2025 pre-tariff buying surge—when consumers accelerated purchases ahead of potential tariff implementation—has created an abnormally weak demand baseline for 2026.

Specific trade measures impacting the auto industry include:

Environmental and emissions regulations present their own complexity. EU CO₂ fleet targets toward 2030 are aggressive, requiring significant EV penetration to meet compliance thresholds. U.S. EPA emissions standards and diverging state-level policies—including California’s zero-emission vehicle mandates—create a patchwork that complicates product planning and distribution strategies.

Possible changes in U.S. policy following election cycles could reshape investment plans dramatically. Modifications to EV tax credits have already demonstrated their power to accelerate or decelerate adoption. Any rollback of climate regulations would shift the calculus for battery plant investments, assembly site locations, and charging infrastructure deployment.

For supply chain design, the implications are clear:

- Nearshoring to Mexico remains attractive but carries policy risk

- Localization of critical components in the U.S. and Europe is accelerating

- Businesses must model multiple policy scenarios in network planning

The bottom line: integrate regulatory forecasting into capital planning, M&A decisions, and long-term contracts with Tier 1 and Tier 2 suppliers. Treating policy as a compliance afterthought is no longer viable.

The EV transition: from hyper‑growth expectations to a managed plateau

The EV adoption trajectory is undergoing a significant correction. After years of aggressive forecasts and heavy capital deployment, the industry is confronting a reality where electric vehicle penetration is growing from a low base but falling short of early-decade projections in major markets.

Current EV penetration as a share of new light-vehicle sales tells the story:

- United States: Approximately 7.5% in 2025, projected to decline to 6% in 2026

- Europe: Subdued demand as stimulus-driven incentives fade

- China: Heading into contraction as governmental incentives expire and tax policies tighten

The decline in U.S. EV share is driven specifically by the expiration of federal EV tax credits, which previously enabled ultra-low lease payments that attracted deal-seeking consumers rather than committed EV enthusiasts. This reveals a critical distinction: subsidized lease incentives masked weak underlying consumer preference for electric vehicles themselves.

For OEMs and suppliers who invested heavily in EV platforms, battery facilities, and dedicated production lines, the slower volume ramp-up creates serious profit and cash flow challenges. Capital deployed against aggressive adoption curves is now generating lower returns, and the payback periods on these investments are extending.

The pain points blocking faster EV adoption are well understood across the industry:

- Up-front pricing remains a barrier despite falling battery costs

- Charging infrastructure density is insufficient outside major metro areas

- Residual-value uncertainty complicates leasing and remarketing models

- Battery raw material costs remain volatile, exposing supply chain risks

Companies are recalibrating their portfolios in response. The industry is experiencing a strategic pivot toward hybrids and range-extended electric vehicles as pragmatic alternatives. Toyota’s strategic focus on hybrids and next-generation battery development has delivered industry-leading EBIT margins, outpacing competitors that pursued more aggressive BEV-exclusive strategies.

Strategic responses for businesses:

- Revisit EV capacity commitments and phase investments against realistic adoption curves

- Form battery and software partnerships rather than building everything in-house

- Redesign dealer sales processes for EV education and customer conversion

- Build EV-specific aftersales capabilities, including battery diagnostics and high-voltage service

The rise of software‑defined vehicles and data‑centric business models

Software defined vehicles represent one of the most significant structural shifts in automotive industry history. The concept is straightforward: vehicles built around centralized compute architecture, continuous over-the-air updates, and the ability to monetize features throughout the vehicle lifecycle rather than only at point of sale. For businesses, this shift creates both existential threats and substantial new opportunities.

Leading players—including Chinese OEMs and tech-oriented manufacturers—are using SDVs to fundamentally change competitive dynamics. Advanced human-machine interfaces, including unified dashboards, multi-screen layouts, and panoramic head-up displays, are rapidly becoming standard equipment. Generative AI deployment in vehicles is expanding, with OEMs implementing sophisticated voice assistants and infotainment systems. Industry projections suggest that by 2031, approximately 28 million vehicles will feature generative AI-powered chatbots.

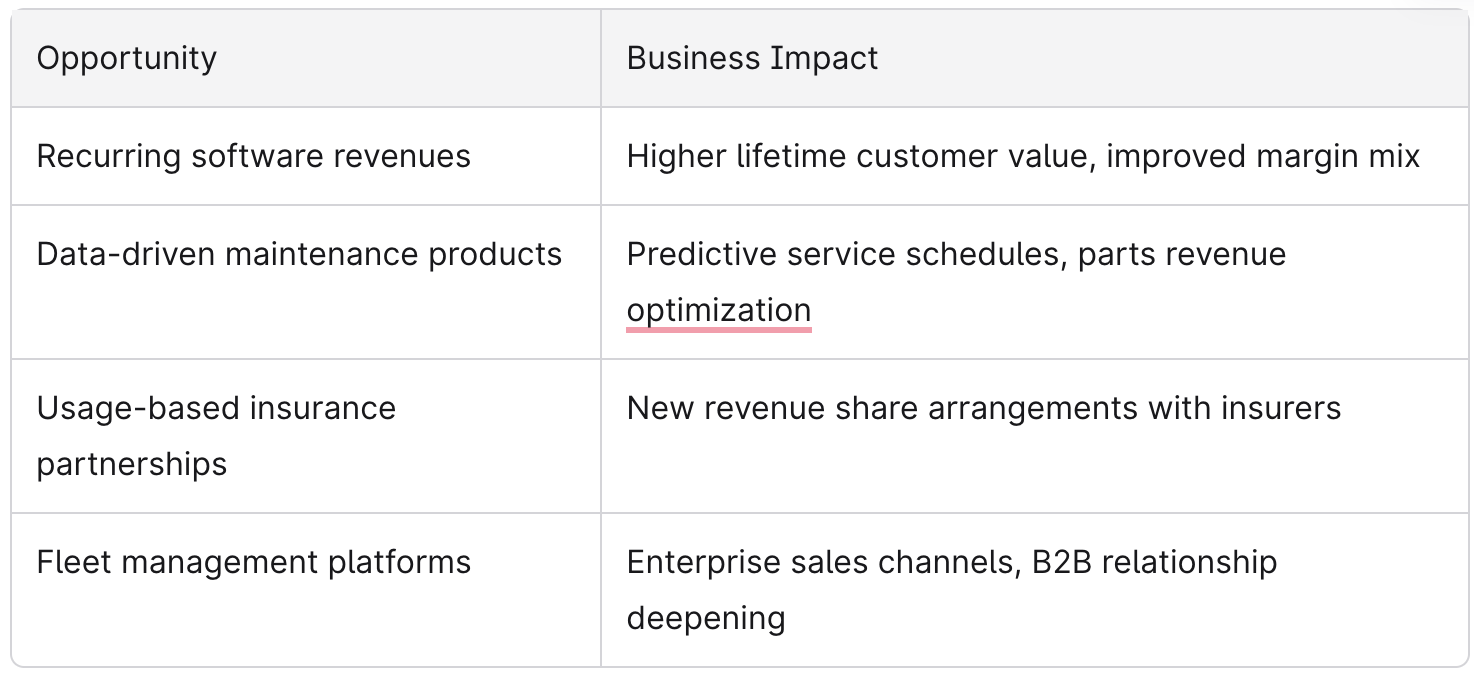

The business model implications are significant. SDVs unlock high-margin revenue streams through:

- Connected vehicle services sold via subscription

- Advanced driver assistance systems features activated post-purchase

- Performance and range upgrades delivered over-the-air

- Usage-based insurance partnerships leveraging real-time vehicle data

- Fleet management platforms backed by continuous telemetry

However, traditional OEMs and dealership networks face real challenges. Legacy electrical/electronic architectures, fragmented software stacks, and sales models not designed for ongoing digital upsell create friction. Many dealers lack the training and incentive structures to support software revenue capture.

Opportunities for 2025–2030:

The organizational shifts required are substantial. Businesses need to build in-house software teams or secure strategic technology partnerships. Cloud and cybersecurity provider relationships become essential. Aftersales contracts must be updated to reflect digital service delivery. Dealer staff require retraining to support and sell digital features.

The technology transformation is happening now. Companies that delay risk falling behind competitors who capture early-mover advantages in software-centric customer relationships.

Competition from China and evolving global supply chains

Chinese OEMs and suppliers have built formidable competitive advantages over the past 10–15 years. Their leadership in EV platforms, battery technology, and cost-efficient manufacturing now represents a structural challenge for legacy automotive companies globally.

The competitive dynamics are stark. Chinese brands are expanding aggressively into Europe, Latin America, Southeast Asia, and the Middle East. Their vehicles often carry price advantages of 20–30% versus comparable offerings from established OEMs, creating intense pressure on competitive pricing across segments. Battery leadership remains firmly concentrated in China, with CATL commanding market dominance and Chinese manufacturers emerging as leaders in advanced manufacturing techniques like magnesium thixomolding.

For non-Chinese OEMs, importers, and dealer networks, the implications are serious:

- Pricing power erosion as Chinese EVs set new price expectations in entry-level and mid-market segments

- Accelerated product refresh requirements to remain competitive on features and technology

- Potential loss of entry-level segments where cost competitiveness is paramount

The industry is also facing excess battery capacity as Chinese production expansion outpaces global demand growth. This creates both risk and opportunity—downward pressure on battery costs benefits all EV manufacturers, but it also strengthens Chinese suppliers’ market position.

Supply chains are being reconfigured in response. Diversification away from single-country dependency is now a strategic imperative. Automotive companies are pursuing:

- Increased localization of battery and component manufacturing in North America and Europe

- More regionalized production footprints aligned with end-market demand

- Alternative suppliers in India, Southeast Asia, and Eastern Europe

- Vertical integration into critical raw materials

Practical strategies for response:

- Pursue partnerships and joint ventures with Chinese technology leaders where trade policy permits

- Launch aggressive cost-reduction programs targeting manufacturing efficiency and platform consolidation

- Adopt modular platform strategies that enable rapid localization across regions

- Evaluate selective market exits where competitive position is untenable and market entries where rising competition creates acquisition opportunities

These decisions belong to executives responsible for sourcing, market expansion, and competitive positioning—not to consumers choosing among brands.

Labor, automation, and the future of automotive operations

The labor landscape in 2024–2025 presents significant challenges for automotive businesses. Skilled-worker shortages in engineering and software roles persist across markets. Union negotiations in North America and Europe have resulted in substantial wage increases. Manufacturing labor costs are rising across traditional production hubs, fundamentally altering cost structures.

Recent labor agreements at major OEMs and suppliers have pushed companies to accelerate automation and productivity initiatives. The economics of manufacturing are shifting, with automation investments becoming more attractive as labor costs rise and technology capabilities advance.

Concrete examples of automation and digitalization transforming operations include:

- Robotics in final assembly achieving higher precision and consistency

- AI-assisted quality control reducing defect rates and inspection costs

- Autonomous material handling in plants and logistics centers

- Digital twins enabling virtual production planning and optimization

- Predictive maintenance reducing unplanned downtime

These changes are reshaping the skills mix required across the industry. Demand for traditional assembly workers is declining while demand for technicians who can program, maintain, and supervise automated systems is increasing.

The impact extends beyond manufacturing. Dealer and aftermarket networks face their own pressures:

- Consolidation of small dealerships unable to invest in technology and training

- Increasing centralization of back-office functions through shared services

- Urgent need for technicians trained in EV high-voltage systems, ADAS calibration, and software diagnostics

Legacy memory chips are scheduled to be phased out by 2028, creating a narrowing window for automakers to redesign systems and secure supply commitments. This timeline constraint makes agile sourcing strategies and deep supplier partnerships critical.

Workforce strategy recommendations:

- Implement reskilling programs that transition employees into higher-value roles

- Form partnerships with technical schools and universities for talent pipelines

- Integrate change management when introducing advanced automation

- Align labor and automation roadmaps with broader product and capacity strategies

Fragmented, plant-by-plant decisions on automation will not deliver the integrated productivity improvements the industry needs. Strategic workforce planning must be a C-suite priority.

Trust, brand reputation, and customer expectations in a shifting market

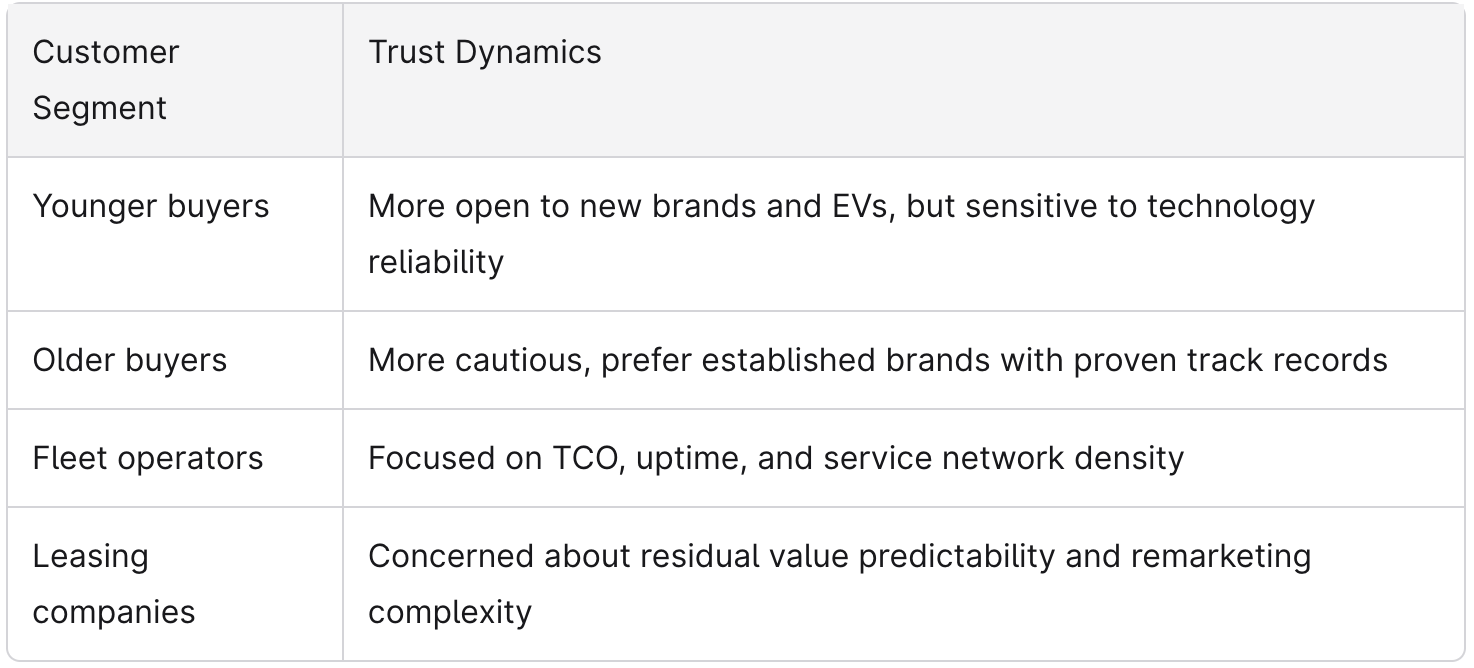

Trust and reputation indicators for the automotive industry have softened in recent years, even as vehicles have become more technologically advanced. This paradox reflects the growing complexity of modern vehicles and the elevated expectations of both retail and fleet customers.

High-profile recalls, software glitches, and EV-related concerns—including range anxiety, battery fire incidents, and degradation uncertainty—are influencing brand perception. These issues directly impact fleet and retail ordering decisions, with buyers increasingly scrutinizing reliability and total cost of ownership before committing to new platforms.

The trust challenge varies across segments:

This segmentation matters for marketing spend and dealer operations. Brands need differentiated messaging and support strategies for distinct customer groups.

Transparent communication around recalls, software updates, and data privacy has become essential. Examples of poor crisis handling—delayed disclosures, confusing messaging, or inadequate remediation—damage brand equity that takes years to rebuild. Conversely, proactive communication and rapid response can actually strengthen customer relationships.

Opportunities to rebuild and enhance trust:

- Robust warranty and service propositions that reduce customer risk

- Clear EV education programs for fleet managers and retail consumers

- Consistent omnichannel experiences across online research and physical dealership touchpoints

- Transparent data privacy policies that address connected vehicle concerns

- Proactive software update communication that emphasizes improvements rather than fixes

This guidance is directed at OEM, distributor, and dealer leadership teams focused on long-term brand equity—not consumer advice on which brand to choose.

Strategic priorities for automotive businesses: 2025 action plan

The themes explored throughout this article point to a consistent conclusion: the automotive industry is navigating a period of structural change that demands integrated strategy rather than isolated tactical fixes. Economic uncertainty, regulatory volatility, technology transitions, and competitive pressure from new entrants are converging simultaneously.

Strategic priorities for 2025:

- Protect cash and profitability

- Prioritize margin over volume; resist the temptation to chase share through unsustainable incentives

- Build scenario-based planning capabilities for tariff and policy volatility

- Rebalance ICE/EV/hybrid portfolios

- Extend profitable combustion platforms where consumer demand supports

- Calibrate EV capacity commitments to realistic adoption curves

- Prioritize hybrids and plug-in hybrids for segments where charging infrastructure remains inadequate

- Regionalize supply chains

- Reduce single-country dependency, particularly for critical components and batteries

- Model multiple policy scenarios in network planning and supplier contracts

- Pursue alternative suppliers in diversified geographies

- Build software defined vehicle capabilities

- Invest in centralized compute architecture and OTA update infrastructure

- Develop or partner for software talent and cybersecurity capabilities

- Create subscription and feature monetization strategies for the vehicle lifecycle

- Invest in workforce transformation

- Align reskilling programs with automation roadmaps

- Build partnerships with technical education institutions

- Prepare dealer networks for EV, ADAS, and software service requirements

- Strengthen brand trust and transparency

- Implement proactive communication protocols for recalls and updates

- Invest in customer education, particularly for EV and connected vehicle features

- Ensure consistent omnichannel experience across digital and physical touchpoints

Near-term vs. medium-term planning:

Define clear 12–24 month moves versus 2026–2030 bets. Near-term actions should focus on cost protection, inventory optimization, and quick-win efficiency improvements. Medium-term investments should target technology platforms, workforce capabilities, and market positioning for the years ahead.

The industry outlook is marked by uncertainty, but uncertainty is not an excuse for paralysis. Businesses that act early on cost structure, technology partnerships, and operating model transformation are best positioned to capture growth and defend margins as market dynamics continue to evolve. The future belongs to companies that treat this moment as an opportunity for strategic differentiation rather than a challenge to be merely survived.

Key takeaways

- The U.S. auto market is stabilizing at 16 million units annually—a sustainable baseline that reflects genuine consumer demand

- EV adoption is decelerating as subsidies expire; expect 6% market share in 2026 versus previous growth projections

- Trade policy and significant tariffs are now core strategic variables requiring scenario planning, not compliance afterthoughts

- Software defined vehicles unlock recurring revenue opportunities but require organizational transformation

- Chinese brands and alternative suppliers are reshaping competitive pricing dynamics globally

- Workforce strategy must align with automation investments and new technology skill requirements

- Businesses that act early on cost, technology, and operating model transformation will outperform in the years ahead

The evolving landscape of the auto industry demands that leaders move beyond reactive decision-making toward proactive strategic positioning. The insights in this automotive industry outlook should inform your planning discussions, capital allocation decisions, and competitive strategies for the challenging and opportunity-rich period ahead.

Ready to transform your automotive lead generation? Driftrock powers lead generation for 65% of the automotive industry, helping 80+ brands across 24 markets generate over 1.7 million leads annually and enable £1.8 billion in vehicle sales. Our platform automatically validates leads, routes them to the right dealers, and tracks performance from click to sale, saving marketing teams an average of 3 years and 11 months in time whilst cutting costs by up to 50%.

Whether you're looking to increase lead volume, improve conversion rates, or prove ROI, we've built the tools automotive marketers actually need. Book a demo to see how we can help you drive better results from your marketing spend.